Lesson #7 of 99: MOIC and IRR are Different Things. And it Matters

At CoVenture we’ve recently brought on two senior partners. I’m honored to begin working with them, and we’ll likely announce who they are later in the Fall.

But bringing those two partners on has forced me to begin thinking about the speed of our growth.

Both of our new partners left positions at larger firms to come on board and aren’t trying to play in a sand box for very long. They don’t just expect us to grow, but they also expect us to grow quickly. They expect us to focus on our IRR.

In the past, I’ve been very patient—likely because I really don’t know what I’d be doing other than CoVenture, and also because I’m fairly satisfied with where we’ve come to date.

But bringing new people on, bringing new investors on, and answering to other constituents has forced me to think about how we can increase our rate of growth.

MOIC Versus IRR

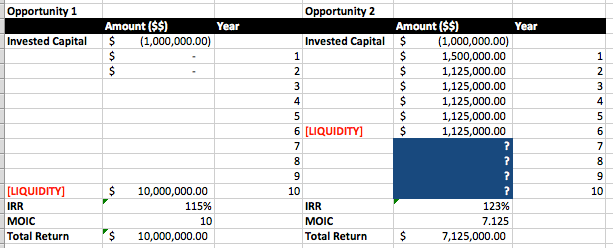

MOIC stands for “multiple on invested capital.” If you invest $1,000,000 and return $10,000,000 in 10 years your MOIC is 10x. If you invest $1,000,000 and return $10,000,000 in 3 years your MOIC is still 10x.

But IRR is different, and often more important. IRR measures your financial return in respect to time. Investors think about IRR, because when they invest $1,000,000 with a 10 year lock up, they are also investing the opportunity cost of everything they could have been doing with that money during those 10 years. (If putting money into the stock market would have earned them 10% year over year, and you’re only offering an 8% return year over year, it’s not worth making the investment. Even if your MOIC in a bunch of years would have been 100X).

Employees and investors often think similarly, because employees are investing their opportunity cost into your company. So your employees will think about IRR over MOIC just like your investors will.

So imagine there are two opportunities:

- The first returns $10mm on a $1mm investment in 10 years.

- The second returns $7,125,000 in 6 years.

The MOIC of Opportunity #1 is higher, but the IRR of Opportunity #2 is more attractive. In most cases, investors will pick Opportunity 2. Employees will pick opportunity 2 assuming they feel like they’ll be able to score a similar opportunity after year 6. (Sometimes MOIC will matter more because the chances of finding another high IRR opportunity is low. But I wouldn’t count on it).

This means the speed of growth matters.

Why do So Many Founders Focus on MOIC?

One reason might be that when founders raise rounds of financing, they give liquidation preferences to investors that are based on MOIC over IRR. They are therefore more focused on protecting against MOIC downside risk.

Founders also don’t know if they’ll be able to find another high-growth opportunity after the sale of their company. An IRR beyond that sale is not guaranteed and their calculation might look more like this:

And finally, the ethos of MOIC is often sexier.

In thinking about growth, it often becomes a balancing act of calculating patience and stability against an attractive and high IRR opportunity.

It’s important to realize that speed of growth has a lot of external motivators, not all of which are good for the company—but sometimes are unavoidable.